How to Choose a Mortgage Lender | Pay Attention to 1-Star Reviews

At Best Company, we believe better data leads to better decisions.

We recently performed an analysis of more than 480 1-star mortgage lender reviews, and have determined common themes and complaints from customers, providing you with reliable data to navigate choosing the best mortgage lender.

The most common customer complaints include the following:

Poor customer service

Lack of transparency

Slow process or delays

Lender errors

High rates or fees

Borrower didn't qualify

.png)

Because this is an overview of general complaints, all specific company and reviewer names are removed. To better understand a specific company’s feedback, read its reviews.

Poor customer service — 56%

Fifty-six percent of 1-star reviews mention poor customer support.

What are the common complaints about customer service?

1. Company representatives were difficult to reach.

- Calls and/or emails weren’t returned.

- Delayed response to calls and/or emails.

- Automated, rather than personal, responses.

- No response after an application was completed.

- No response after the applicant was denied a loan.

- Communication was poor between loan officers and underwriters.

- Communication was poor to other vendors like title companies and real estate agents.

.png)

2. Consumers didn't have a consistent contact point.

- Point of contact changed multiple times.

- Point of contact went on leave or vacation without telling the customer and failed to provide an alternate contact.

3. Company representatives weren’t on the same page.

- Customers continued to receive loan offers after their loan was denied.

- Customers were bombarded with loan offers, but communication was halted when an offer was pursued.

- Delays in re-verifying information over the phone.

- Multiple representatives within the same company asked for the same documents several times.

4. Company representatives were unhelpful.

- Lacked training and knowledge.

- Provided incorrect or vague information.

- Rude communication.

- Local support was good; corporate support was bad — difficulties in escalating issues to higher ups.

.png)

How can you avoid bad customer service?

Test the system.

You can test out more than one lender's customer service before committing. Call or email multiple lenders with your questions and see who responds first. If you’re having a hard time getting in touch with company representatives, this could be a good indication that you won’t have good experiences with customer service later on.

Some things to consider:

- Which companies send you a personal response rather than an automated one?

- Which companies are available over the weekends?

- Which companies are willing to work with you on a holiday?

Be upfront.

Define and share your communication boundaries and expectations as you shop for a lender. If you know how you’d prefer to be communicated with, don’t be afraid to look for it and ask for it.

Some things to consider:

- How would you like to communicate?

- How would you like to be communicated with?

- How often do you want to be notified throughout the mortgage process?

- How quickly do you expect responses to emails, calls, or text messages?

Be understanding, within reason.

Though you may want to close as quickly as possible, keep in mind that your loan officer is a person too, and typically someone who is trying their best to do their job. Just like you, loan officers get sick, take vacations, and have families. Plus, they have other clients to assist. While this doesn’t excuse miscommunication or lack of communication, patience and understanding can go a long way.

Provide all of your documents as quickly as possible.

Often, loan officers are waiting to complete the underwriting process because the borrower has not returned documents the loan officer has requested. The faster you can provide your loan officer with the required documentation, the faster you can get to closing.

You should be prepared to provide the following documents:

- Tax returns

- W-2s or pay stubs (or any other proof of income)

- Bank statements

- Proof of assets

- Credit history

- Employment verification

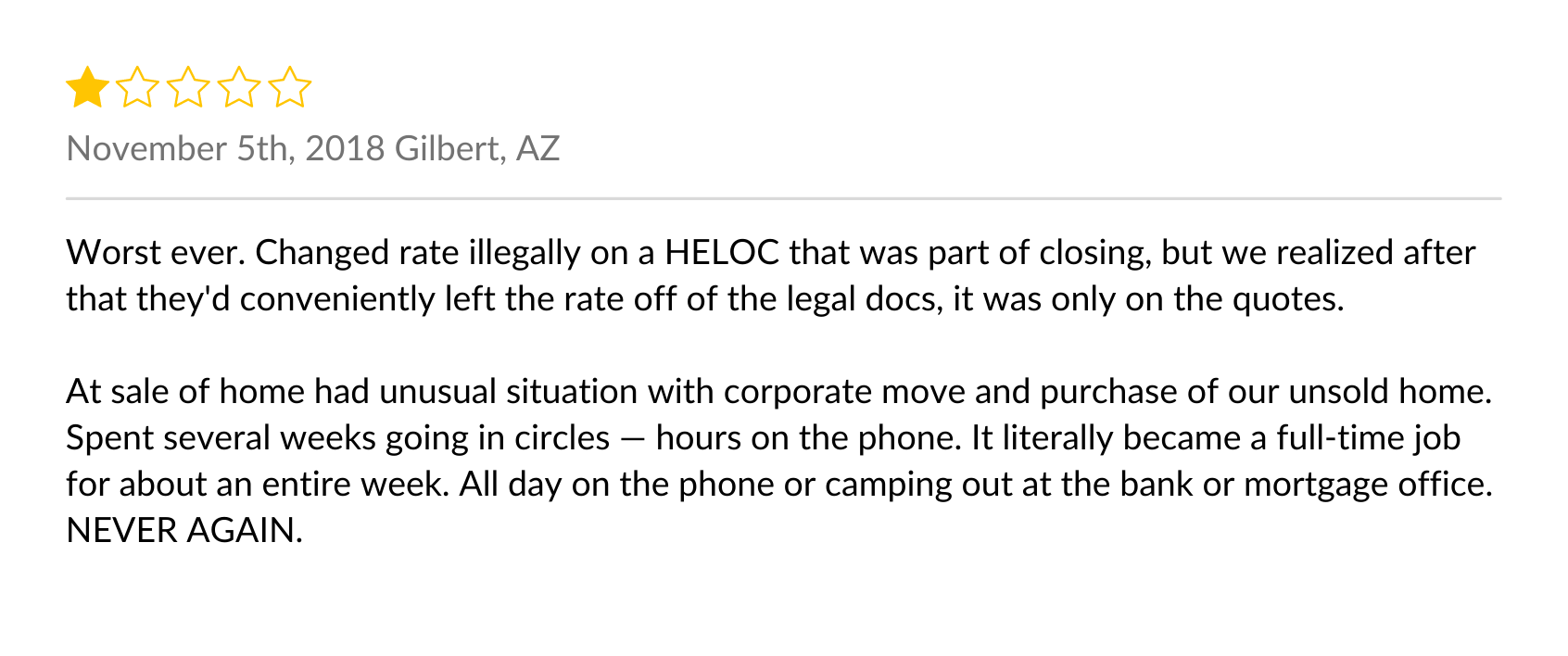

Lack of transparency — 41%

Forty-one percent of 1-star reviews mention a lack of transparency.

What are the common complaints surrounding lender transparency?

1. The lender didn't follow through on a promise.

- A special offer was advertised but wasn’t honored.

- A company guarantee wasn’t backed.

- A lender credit amount at closing was promised, but it was decreased without notice.

- A waived payment option was offered, but was later denied.

2. The lender didn't adequately inform the borrower.

- Private mortgage insurance (PMI) was added to a loan without explanation.

- Closing costs changed without notice.

- Loan requirements weren’t explained.

- Exact fees weren’t communicated upfront.

.png)

3. The lender was dishonest.

- The agreement of sale was changed without notice.

- Fees were hidden or miscommunicated throughout the loan process.

- A prepayment penalty was hidden within the loan.

- A home was under appraised.

- A home was over appraised to approve a more costly refinance.

- More was charged for escrow even when taxes went down.

.png)

How can you find a transparent and reliable lender?

Do your research.

Read the terms and conditions under any guarantees listed on a company's website. Generally, lenders reserve the right to change guarantees and promotions at any time.

Ask about fees or prepayment penalties. This may not seem like a big deal up front, but you probably won’t like being hit with a fee at closing that you didn’t think you knew about before.

Be transparent.

You may not be able to control the transparency of your lender, but you can control the details you give them. In your loan application and moving forward, share all relevant details that may impact your eligibility for a mortgage.

Many borrowers are disappointed that their lenders don't identify problematic information until it's too late to resolve the issue before the initial closing date. You can avoid such situations by disclosing student debt, tax debt, and all other financial obligations upfront.

Get a second opinion.

An appraiser decides how much your home is worth, and, in turn, the maximum amount the bank is willing to loan you. As the borrower, you are responsible to pay for the appraiser, but you don't have a lot of control around who does it since your mortgage broker hires the appraiser (often through a third-party appraisal management company). The bank's chosen appraiser is the authority on that particular loan. However, you can hire your own appraiser to serve as a second opinion.

Slow process or delays — 18%

Eighteen percent of 1-star reviews mention a slow mortgage process or delays.

What are the common complaints about delays in the process?

1. Too much paperwork was required.

- The loan application was too long.

- The lender required irrelevant information.

- The lender required information to be notarized.

- The lender required information that took too much time to get.

2. Loan approval and closing took too long.

- The lender blamed the delay on underwriting.

- The process should have taken 30–45 days but took 60 days or more.

- The original closing date was postponed.

- The lender was slow to pay property taxes via escrow.

- The seller walked and the buyer lost the earnest money.

.png)

How can you ensure that your loan closes on time?

Gather paperwork ahead of time.

Get a head start on your mortgage by gathering some of the information you'll need before being approved for your loan, including the following, where applicable:

- Tax returns

- Bank statements

- SSNs

- Auto loans

- Student loans

- Credit card debts

- Current mortgage(s)

- Rent payments

- Divorce documents

- Retirement accounts

- Recent income statements

- Down payment gift statement

Lock your rate strategically.

Many lenders offer rate lock options in case rates rise. If a rate lock appeals to you, look for a lender that doesn't charge you for this service and that has an extended rate lock period.

Realtor Daniele Kurzweil asks her clients to consult with her before locking their rate.

"From start to finish, the whole process of buying in NYC takes roughly 90 days. What inevitably happens is that a mortgage broker hears that we have an accepted offer and tells the buyer to lock their rate that day.”

"However,” Kurzweil explains, "that doesn't take into consideration the time it takes to finalize the loan" in her local market, including the following steps:

- 10 days for the contract to be reviewed and the financials of the building to be verified

- 30 days to gather and submit paperwork

- 2–3 weeks for the building representative to review the paperwork

Kurzweil describes the disappointment that can come when things take longer than expected: "All of a sudden, the 60-day rate lock has come and gone and my clients are stuck paying for an extension."

Expect delays.

Some loans will close within a month, but in many cases it can take much longer. If you keep your expectations low, you create space to be pleasantly surprised if the process goes quickly.

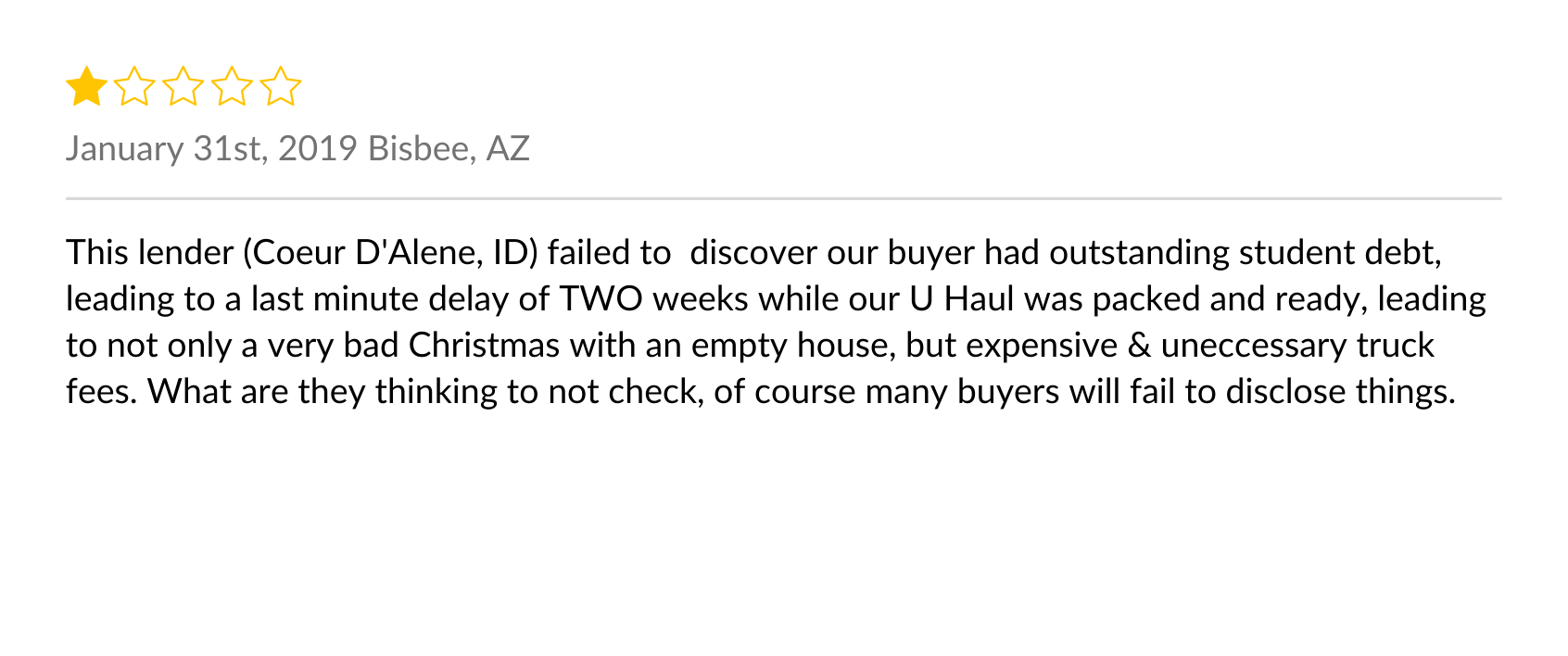

Lender errors — 12%

Twelve percent of 1-star reviews mention lender errors.

What are the common complaints about lender errors?

1. Important financial details were missed.

- A partner's income was left out of a loan.

- The borrower was told that they needed more money down when they didn’t.

- The lender omitted to inform a borrower that a cosigner was needed.

- A student loan account was overlooked.

2. The lender had a typo or misclick.

- Monthly mortgage payments were processed more than once.

- A late payment was charged after a refinance.

- Multiple hard credit pulls were performed in one week.

- Bank account information was recorded incorrectly.

- Names were recorded incorrectly.

3. The lender incorrectly handled escrow funds.

- Funds were misplaced into escrow.

- Property taxes were assessed incorrectly.

- Communication with the city was executed poorly.

.png) How can you avoid errors in the loan process?

How can you avoid errors in the loan process?

Repeat yourself.

Be willing to share and re-share important details relevant to your loan, even if you've already included them in your loan application, including names, birth dates, assets, and debts. Don't assume your lender will catch any discrepancies because they might not, or they might not catch it until it's too late.

Audit paperwork.

Where possible, look over the paperwork before it's sent to underwriting and again before closing documents are finalized. Work with your loan officer to do this face to face if there's a branch location near you, or over email, video chat, or a secure document sharing platform.

Verify your taxes and insurance.

To make sure your property tax payments from your mortgage servicer are going through, call the city or visit the property appraiser’s website yourself to confirm. You may also want to contact your home insurance provider, as yearly home insurance premiums are usually bundled in your escrow payments.

High rates or fees — 8%

Eight percent of 1-star reviews mention high rates or fees.

What are the common complaints about rates and fees?

1. The lender charged too many fees.

- Fees and closing costs were higher than quotes from other lenders.

- The lender's title company charged more than others.

- Escrow fees were increased after acquiring the loan.

- A fee was charged for locking into a rate.

- The lender charged borrowers to submit a payment.

- Certain fees weren’t reimbursed when a loan didn’t close — building survey, appraisal, and home inspection fees.

.png)

2. The rates were too high.

- Interest rates were high despite a borrower's excellent credit.

- Interest rates jumped arbitrarily while market rates went down.

- The lender didn't offer a rate lock or guarantee.

- New terms required a higher interest rate.

.png) How can you secure low rates and fees?

How can you secure low rates and fees?

Be aware of standard fees.

It's the norm for buyers to pay for some services out of pocket before obtaining a loan.

You'll be responsible for some or all of the following fees, most of which are non-refundable:

- Appraisal

- Title insurance

- Home inspection

- Credit report

- Documentation

- Land survey

Some fees, such as origination fees, escrow fees, and home insurance, are generally bundled within your loan amount to be paid off over time. Plan to spend anywhere from 2 to 5 percent of the purchase price of the home in closing costs.

Prepare financially before you buy.

To improve the interest rates for which you qualify, take steps to improve your credit. Pay off your other loans and debts where possible.

Shop around.

You can compare quote estimates from several mortgage lenders before initiating a hard credit pull and before committing to one. Getting multiple quotes from multiple lenders can help you explore how your mortgage terms may change based on down payment, credit score, location, and home value with online financial calculators.

Borrower didn’t qualify — 5%

Five percent of 1-star reviews mention instances where a borrower didn’t qualify for a mortgage loan.

What are the common complaints about being denied for a loan?

1. The borrower "should have" been approved.

- The lender didn't accept 1099 income (self-employment or independent contractor income).

- A manufactured home didn’t qualify for financing.

- The lender advertised that borrowers with bad credit would get approved, but they were denied.

2. The borrower was given false hope.

- Pre-approval was offered but the borrower was denied upon applying.

- The borrower was approved all the way to closing, including signing and submitting final disclosure and closing costs, then denied due to an employment gap.

What do you do if you're denied for a loan?

What do you do if you're denied for a loan?

Don't take it personally.

If you've been turned down for a mortgage purchase, even at the last minute, it doesn't mean the lender doesn't like you. These decisions are almost all about numbers.

Reapply.

Your eligibility for a particular loan type can improve over time as you improve your credit and debt-to-income (DTI) ratio, among other factors. Plus, sometimes lenders change their standards or add additional mortgage products that may better fit your situation. Lenders often approve applicants with subprime credit for FHA loans.

Don't let a loan rejection from one lender stop you from applying elsewhere.

Focus on your credit.

Credit scores are probably the single most important factor in what rates and mortgage programs a borrower will be offered, according to Terence Michael of Omni-Fund Mortgage Brokerage. "Make sure that you do not owe more than 30 percent of the total available credit on any one of your credit cards, even for a day," Michael advises. "This is one of the best hacks for either boosting your credit score or keeping it from dipping right when it’s checked by a lender or bank."

If you are denied for a mortgage, taking the time to build or repair your credit can help ensure an approval next time.

"Keep in mind that you cannot fix your credit overnight," explains credit industry analyst Greg Mahnken at Credit Card Insider. "It takes time to build a strong credit file and demonstrate your worthiness as a borrower. You’ll need to demonstrate that you can make payments on time, keep your utilization low, minimize your applications for new credit, and have a healthy credit mix. The age of your credit accounts is also a factor, so keep that in mind before closing any credit card accounts."

Other ways to build your credit include using a credit builder loan and adding rent and utility payments to your credit reports. Your loan officer should also have resources to help you improve your credit score.

Top-Rated Mortgage Lenders

Compare top-rated mortgage lenders on BestCompany.com, based on customer reviews.

CompareThe Top Mortgage Lenders Companies

The Top Mortgage Lenders Companies

Related Articles

Mortgage Lenders

Planning to Refinance Your Mortgage? 5 Questions You Sh...

By Guest

April 12th, 2023

Mortgage Lenders

How Much Harder Is It to Get an Investment Property Loa...

By Guest

April 12th, 2023

Mortgage Lenders

When Should You Take Out a Second Mortgage?

By Guest

October 27th, 2022

Get Our Newsletter - Be in the Know

Sign up below to receive a monthly newsletter containing relevant news, resources and expert tips on Mortgage Lenders and other products and services.

We promise not to spam you. Unsubscribe at any time. Privacy Policy